Smartphone Shipments to Drop in 2026 as Memory Shortage Pushes Prices Higher

Global smartphone shipments are now forecast to fall 2.1% in 2026, as surging memory prices drive up manufacturing costs and force handset makers to rethink pricing and product strategies.

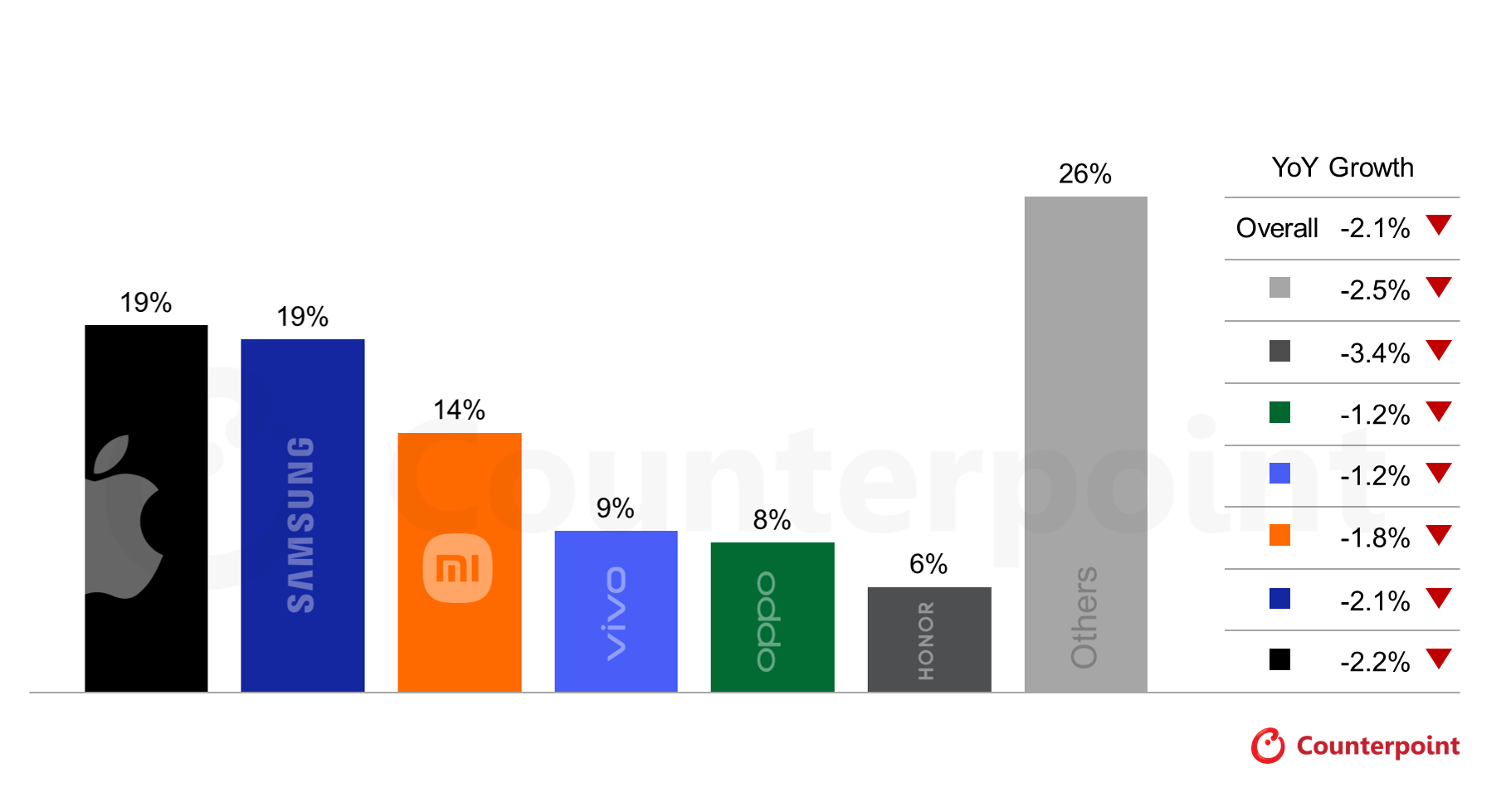

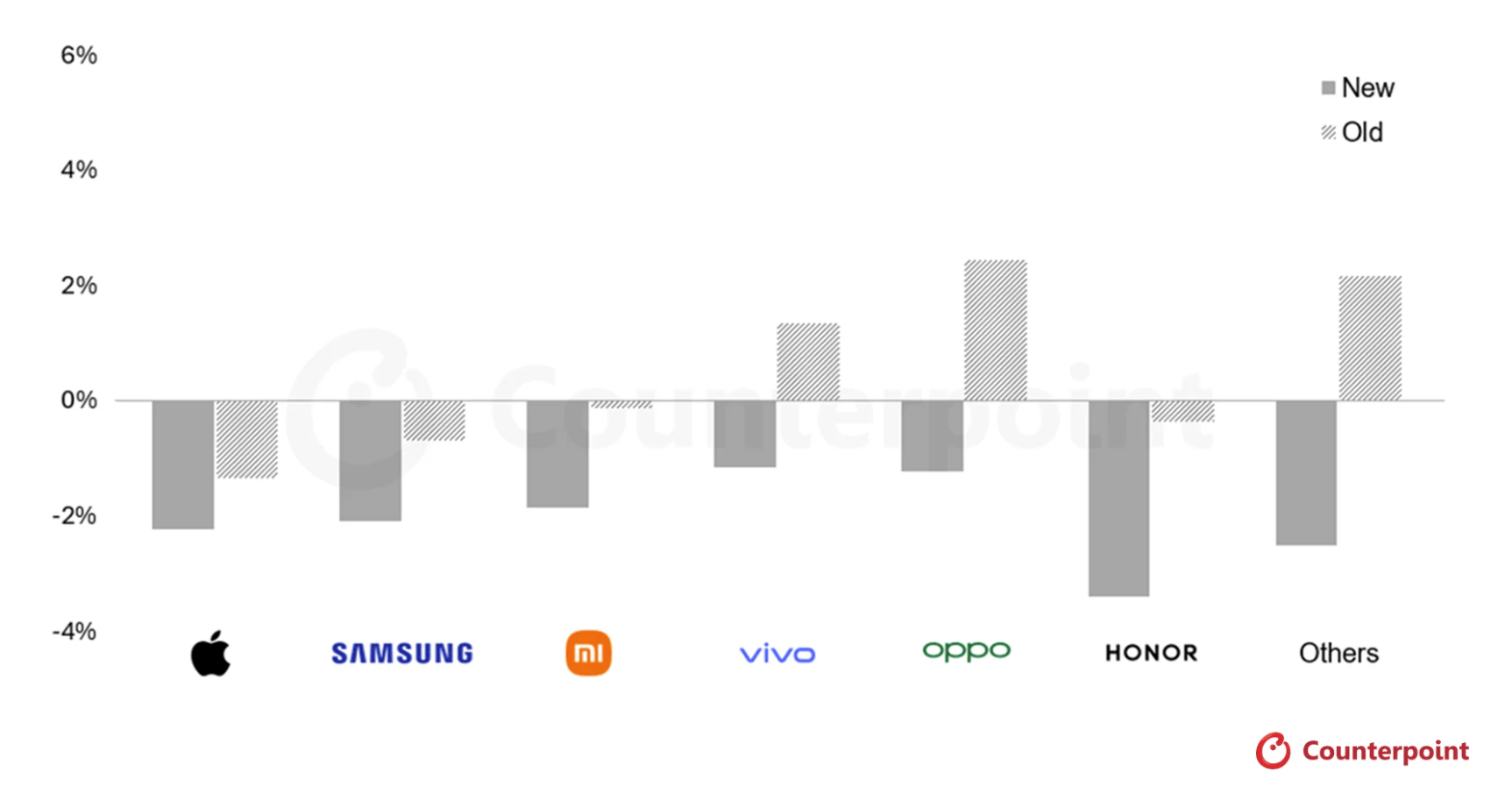

New data from Counterpoint Research shows the outlook has worsened sharply, with the firm cutting its 2026 shipment forecast by 2.6 percentage points compared to earlier estimates.

Chinese manufacturers including HONOR, OPPO and vivo face the largest downward revisions, while the low-end smartphone market is expected to be hit hardest.

The downgrade comes as the global memory shortage, dubbed ‘RAMageddon’, intensifies.

DRAM prices have surged amid fierce competition from AI and cloud data centres, with Samsung, SK Hynix and Micron prioritising higher-margin enterprise customers over consumer devices.

Counterpoint estimates that rising DRAM prices have already lifted smartphone bill-of-materials (BoM) costs by around 25% for low-end handsets, 15% for mid-range models and 10% for premium devices.

Further cost increases of 10–15% are expected through the first half of 2026, with memory prices potentially climbing another 40% by Q2.

“The sub-US$200 segment is being impacted most severely, with BoM costs up 20–30% since the start of the year,” said Counterpoint Research Director MS Hwang. “Price increases of this scale are simply not sustainable at the low end.”

As a result, manufacturers are increasingly trimming their portfolios, cutting back on entry-level SKUs and pushing buyers toward higher-priced models.

Average selling prices are now forecast to rise 6.9% year-on-year in 2026, almost double earlier expectations.

Some vendors are also downgrading specifications to manage costs, including lower memory configurations, older camera modules and reused components.

Others are steering customers to “Pro” variants to protect margins.

Counterpoint says Apple and Samsung are best positioned to weather the turmoil due to scale, vertical integration and strong high-end portfolios.

For smaller players, particularly Chinese OEMs, 2026 is shaping up as a difficult balancing act between market share and profitability.