JB Hi Fi Q3 Numbers See Shares Wobble

JB Hi-Fi Limited’s Q3 FY26 trading update issued today paints a picture of resilient top-line growth battling increasingly tight supply chain and competitive headwinds.

While the headline sales figures remain positive, the broader commentary highlights significant macroeconomic uncertainties that have caused some jitters in the market, with JBH shares sliding roughly 6.8% trading at 240am at $72.46.

Here is a breakdown of what is being reported and said regarding their performance and outlook:

1. The Sales Metrics (Q3 FY26)

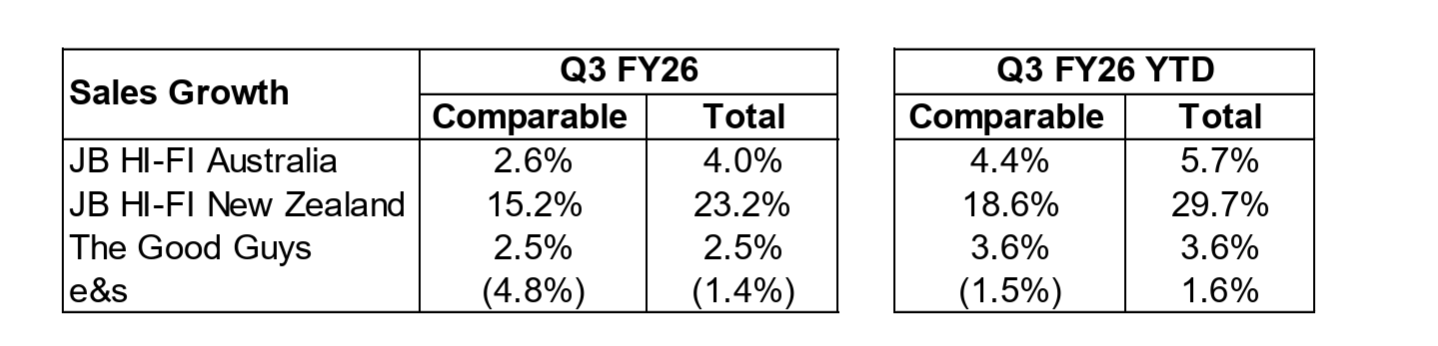

The group sustained its growth momentum across its primary banners compared to the previous year, driven largely by solid promotional execution and steady consumer demand for tech and appliances:

JB Hi-Fi Australia: Total sales grew by 4.0%, with comparable sales up 2.6%.

The Good Guys: Total sales rose 2.5%, showing steady performance in white goods and home appliances.

JB Hi-Fi New Zealand: Continued to be a major growth driver, delivering high double-digit sales increases on both a total and comparable basis.

e&s: The recently acquired premium appliance commercial arm showed modest total sales improvement, though it dragged slightly on negative comparable sales for the quarter.

2. Supply Chain Risks & “Component Cost” Pressures

The major talking point from the update, and the likely driver behind the cautious investor response,is the operational headwinds flagged by Group CEO Nick Wells.

As the retailer enters the crucial end-of-financial-year (EOFY) trading window, management explicitly called out significant supplier component-related cost increases and stock availability shortages, particularly within core technology categories. This comes alongside an overall spike in “heightened competitive activity” as retailers fight harder for tightening consumer dollars.

3. Management Strategy & Market Sentiment

Despite an “increasingly uncertain retail environment,” JB Hi-Fi is leaning heavily on its established retail playbook to preserve margins and market share heading into June. Wells noted that the company will focus on what it can control by:

Leveraging deep supplier relationships to navigate stock shortages.

Sharpening their value proposition to maximize customer demand.

Maintaining tight operational and cost discipline.

Market Reaction: Analysts remain divided. While some investment platforms continue to label JBH a “Buy” with price targets hovering around $85.00—citing the resilience of its multi-brand strategy and stellar first-half performance ($6.1 billion in sales)—broader market sentiment today is focused heavily on the near-term margin risks posed by rising hardware costs and tech product shortages.