Apple Surges as Samsung Stumbles in Global Smartwatch Market Recovery

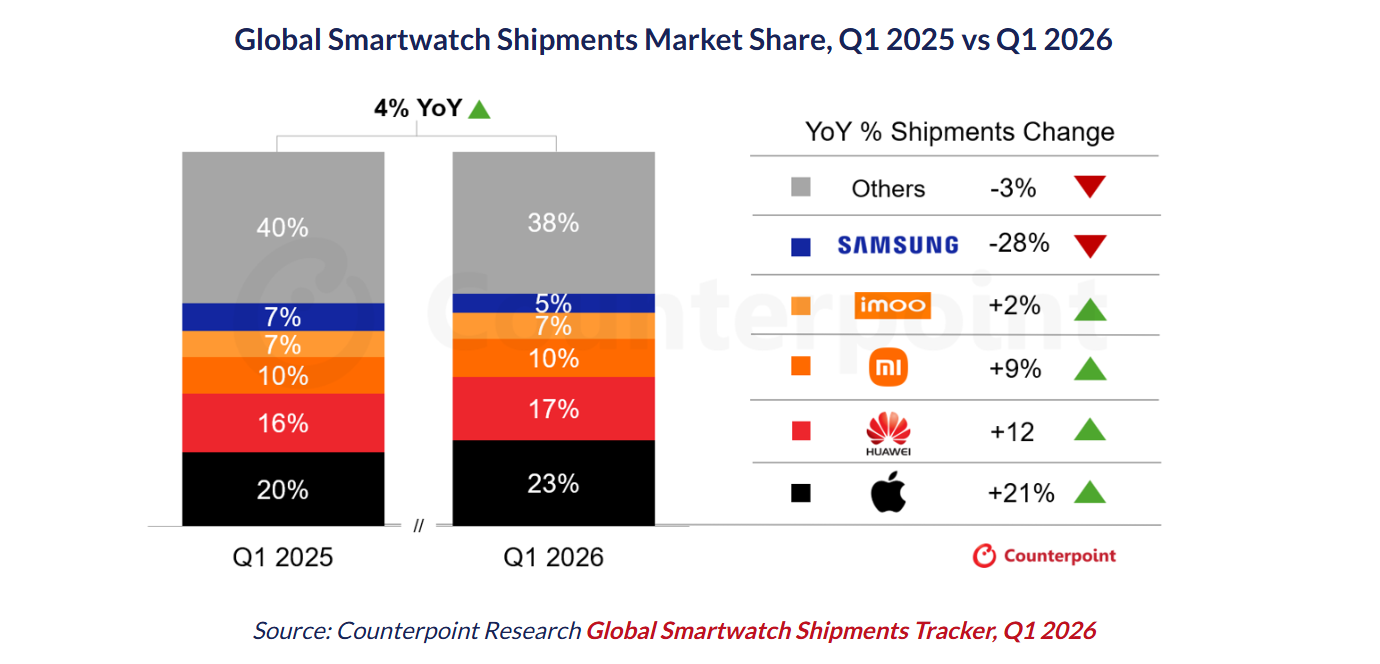

Apple has emerged as the clear winner in the smartwatch market, capturing a dominant 23% share as consumers increasingly trade up to premium health-focused wearables, while Samsung suffered a sharp 28% decline in demand.

New data from Counterpoint Research’s Global Smartwatch Shipments Tracker shows the smartwatch market grew 4% year-on-year in the first quarter of 2026, defying inflationary pressures and broader weakness across consumer electronics categories.

The growth comes as retailers in Australia continue to benefit from rising demand for premium wearables, with consumers increasingly willing to pay more for advanced health-monitoring features and AI-driven functionality.

According to Counterpoint, Apple was the standout performer during the quarter, recording a 21% surge in shipments and capturing the largest share of the global smartwatch market.

The company’s success was driven by a refreshed product portfolio, the launch of the more affordable Apple Watch SE 3, and growing consumer demand for advanced health features.

Counterpoint Research Principal Analyst Anshika Jain said Apple’s momentum was particularly strong outside its traditional North American stronghold.

“Apple has captured the highest shipment share of 23% and emerged as the strongest performer in Q1 2026, driven by the continued success of its refreshed lineup,” Jain said.

“While North America contributed over half of the total shipments of Apple, China and Europe recorded the fastest growth for the brand. The addition of meaningful health upgrades and the affordable SE 3 attracted new buyers.”

The strong performance marks another milestone in the smartwatch market’s recovery following a difficult 2024, when slowing demand and economic uncertainty weighed heavily on sales.

Samsun Watch sales struggling

Analysts say the rebound gathered pace throughout 2025 as manufacturers introduced a wave of new technologies, including satellite connectivity, 5G RedCap support, artificial intelligence capabilities and more sophisticated health-monitoring functions for conditions such as sleep apnoea and hypertension.

Those innovations are now reshaping consumer purchasing behaviour.

The average selling price of a smartwatch rose 6% year-on-year during the quarter as buyers migrated away from basic fitness bands and towards premium smartwatches packed with health and wellness features. The fitness band segment, by contrast, declined by more than 6%.

Demand is increasingly being driven by features such as deep sleep analysis, arrhythmia detection, emotional wellbeing monitoring and AI-powered personal insights.

While Apple celebrated a breakout quarter, Samsung endured one of its weakest smartwatch performances in recent years.

Shipments of the Galaxy Watch range plunged 28% year-on-year, causing Samsung’s global smartwatch market share to fall from 7% to just 5%.

Industry analysts said momentum behind the Galaxy Watch 8 series faded rapidly following the holiday period, while technical shortcomings—including the absence of 5G connectivity available on newer competing devices—also weighed on sales.

Attention is now turning to Samsung’s upcoming July Unpacked event, where the company is expected to unveil new wearable products in an attempt to regain lost market share.

Despite ongoing concerns surrounding memory component shortages and broader macroeconomic uncertainty, Counterpoint believes the smartwatch category remains significantly more resilient than many other consumer electronics sectors.

Higher margins on premium devices have allowed manufacturers to absorb supply chain pressures more effectively, helping shield the category from the severe disruptions experienced elsewhere in the industry.

Although analysts expect memory shortages and economic headwinds to moderate growth during the remainder of 2026, the long-term outlook remains positive.

Counterpoint forecasts the global smartwatch market will continue expanding through the decade, delivering a compound annual growth rate of approximately 3% through to 2030.