Australia’s Unemployment Rate Climbs to 4.3% as Labour Market Shows Signs of Cooling

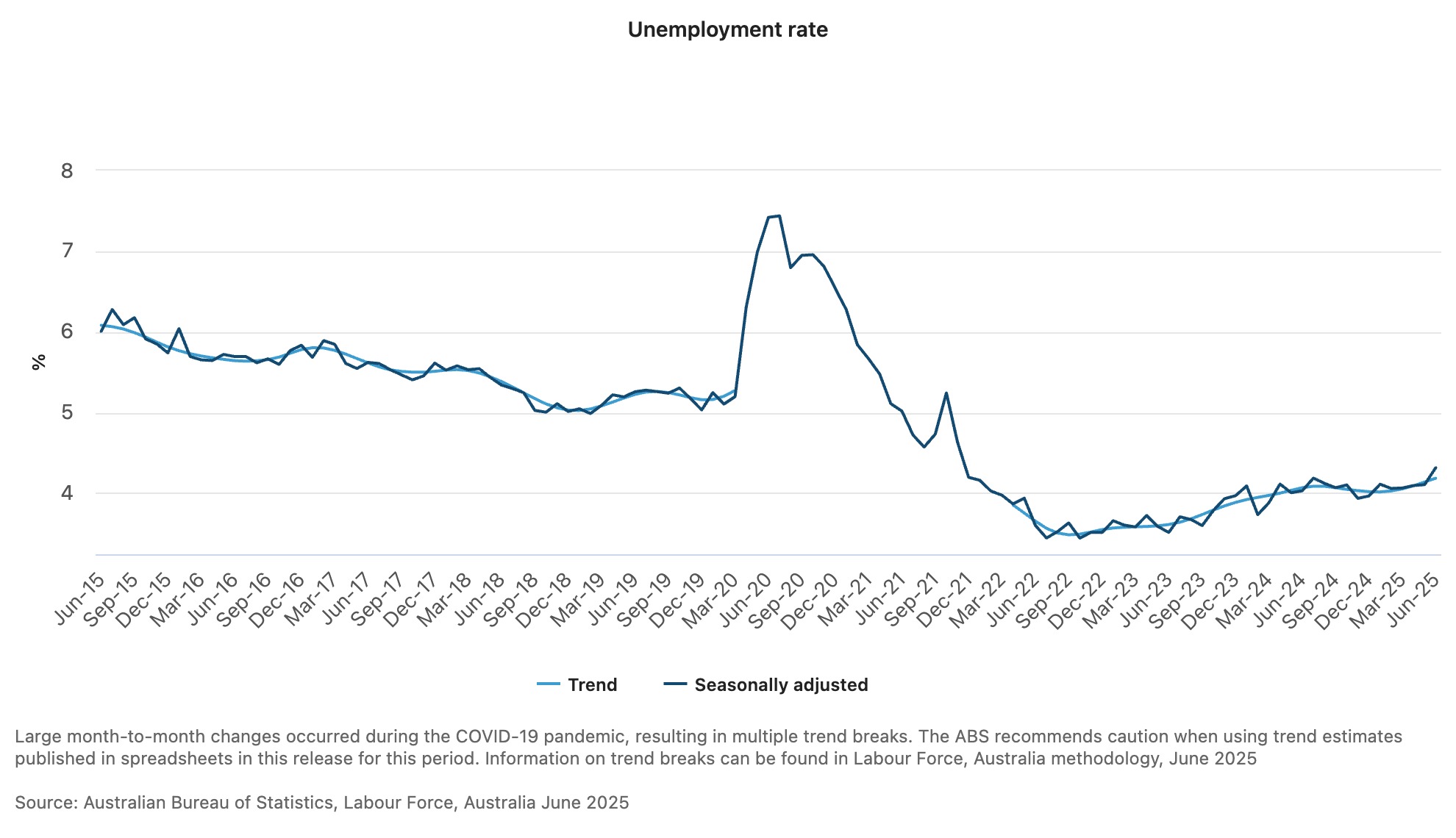

Australia’s unemployment rate rose to 4.3% in June 2025, marking a notable increase from the 4.1% recorded in May and signalling the first significant softening in labour market conditions this year, according to the latest Australian Bureau of Statistics data.

The rise, driven by a 34,000 increase in unemployed people, coincides with growing pressure on the Australian dollar as economic uncertainty weighs on currency markets.

Sean Crick, ABS head of labour statistics, said the unemployment increase reflected labour market cooling after an extended period of tightness.

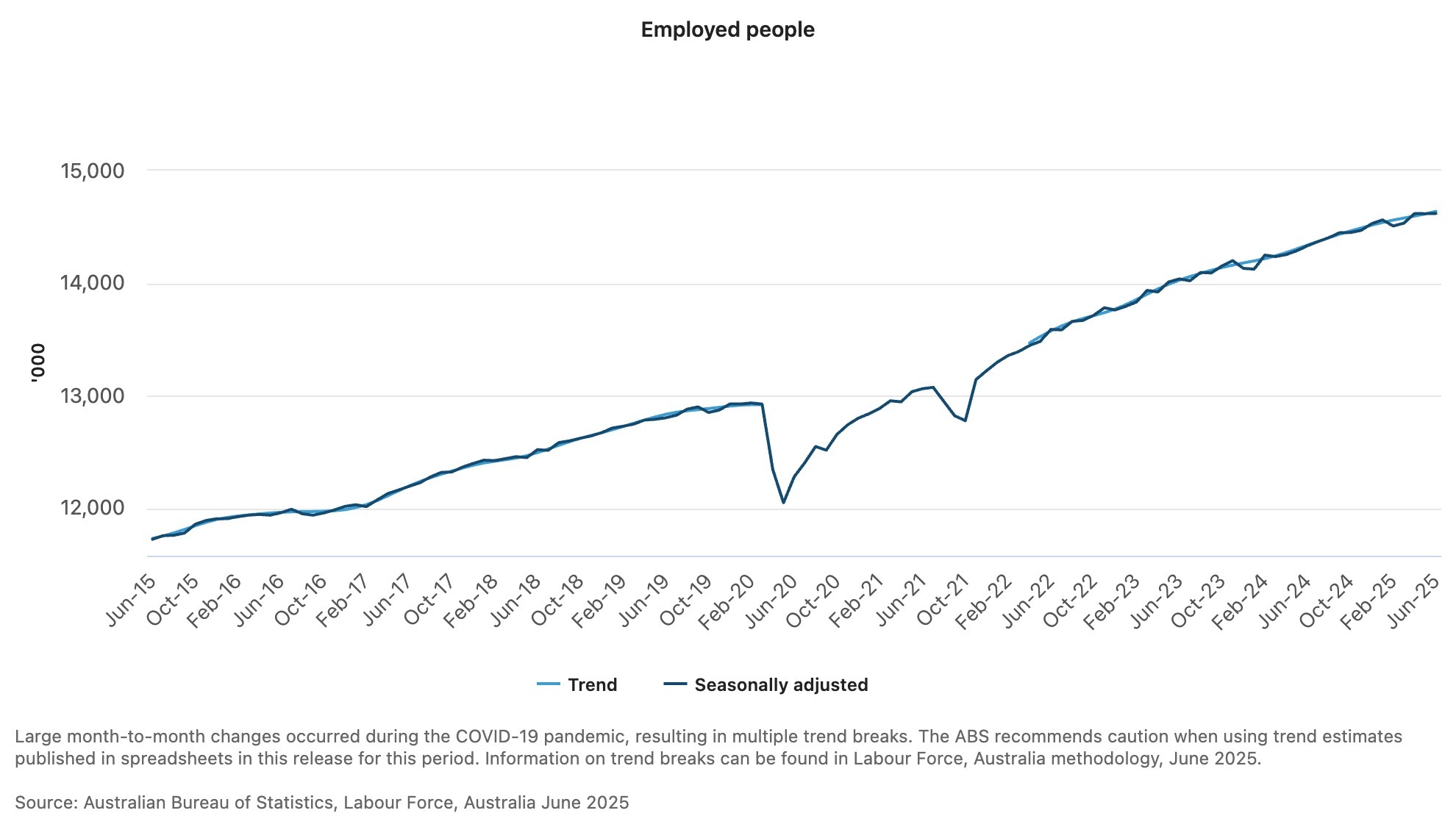

“This month we saw the unemployment rate rise 0.2 percentage points, driven by a 34,000 increase in the number of unemployed people,” Crick explained, noting that employment rose by only 2,000 people in June following a 1,000-person decline in May.

The labour market dynamics revealed significant compositional changes, with part-time employment growing by 40,000 people while full-time employment fell by 38,000.

Despite the unemployment increase, the employment-to-population ratio remained stable at 64.2%, while the participation rate rose to 67.1%, suggesting continued workforce engagement despite softer job creation.

The Australian dollar has faced headwinds amid the labour market softening and global economic uncertainty.

Trading at approximately 0.6522 against the US dollar on July 17, the AUD has strengthened 0.73% over the past month but remains down 3.09% over the past 12 months, reflecting broader concerns about Australia’s economic outlook and delayed monetary policy easing.

Reserve Bank of Australia deliberations on interest rate cuts have become increasingly complex as policymakers balance labour market cooling against persistent inflation concerns.

RBA Assistant Governor Sarah Hunter recently warned that “higher US tariffs will put a drag on the global economy” while noting that increased uncertainty could dampen investment, output, and employment in Australia.

Market expectations for RBA rate cuts have intensified following the June employment data, with some analysts now anticipating action as early as July rather than the previously expected August timeframe.

However, the central bank has maintained a cautious stance, with the most recent monetary policy decision made by a narrow 6-3 majority vote to hold rates unchanged at 3.85%.

The employment deterioration extends beyond headline figures, with hours worked falling 0.9% in June after rising 1.4% in May.

Full-time hours worked declined 1.3%, associated with the 0.4% fall in full-time employees, suggesting a broader weakness in labour demand beyond unemployment statistics alone.

The underemployment rate rose by 0.1 percentage points to 6.0% in June, though it remained 0.4 percentage points below June 2024 levels and 2.7 percentage points below the March 2020 pre-pandemic level.

The combined underutilisation rate, encompassing both unemployment and underemployment, increased but remained historically low by international standards.

Currency analysts note that the Australian dollar’s performance reflects competing pressures from domestic labour market softening and global economic uncertainty stemming from US-China trade tensions.

While a potential RBA rate cut could weaken the currency, analysts suggest that Australia’s commodity export strength and relatively stable economic fundamentals may provide support.

The labour market cooling occurs as the RBA faces complex policy trade-offs between supporting employment growth and controlling inflation pressures.

Despite the unemployment increase, wage growth remains elevated, and productivity growth has not improved substantially, creating challenges for monetary policy settings.

Employment growth over the past year remains robust at 2.0% compared to June 2024, though the pace of monthly job creation has clearly decelerated from earlier in 2025.

The shift toward part-time employment growth may reflect business caution about economic conditions and preference for flexible staffing arrangements.

The currency implications of labour market softening could influence broader economic conditions through import costs and inflation pressures.

A weaker Australian dollar typically increases import prices while supporting export competitiveness, creating mixed effects on domestic economic activity and RBA policy considerations.

Looking ahead, the intersection of labour market trends and currency movements will likely influence RBA policy timing and the broader economic outlook as Australia navigates global trade tensions and domestic economic adjustment pressures in the second half of 2025.