Harvey Norman’s Debt Is Manageable But Potentially Risky

Harvey Norman’s latest full-year results reveal the retailer carrying a substantial, if seemingly easily manageable, debt load.

There is cause for both optimism and pessimism, depending on what figures and possible future scenarios you want to focus on.

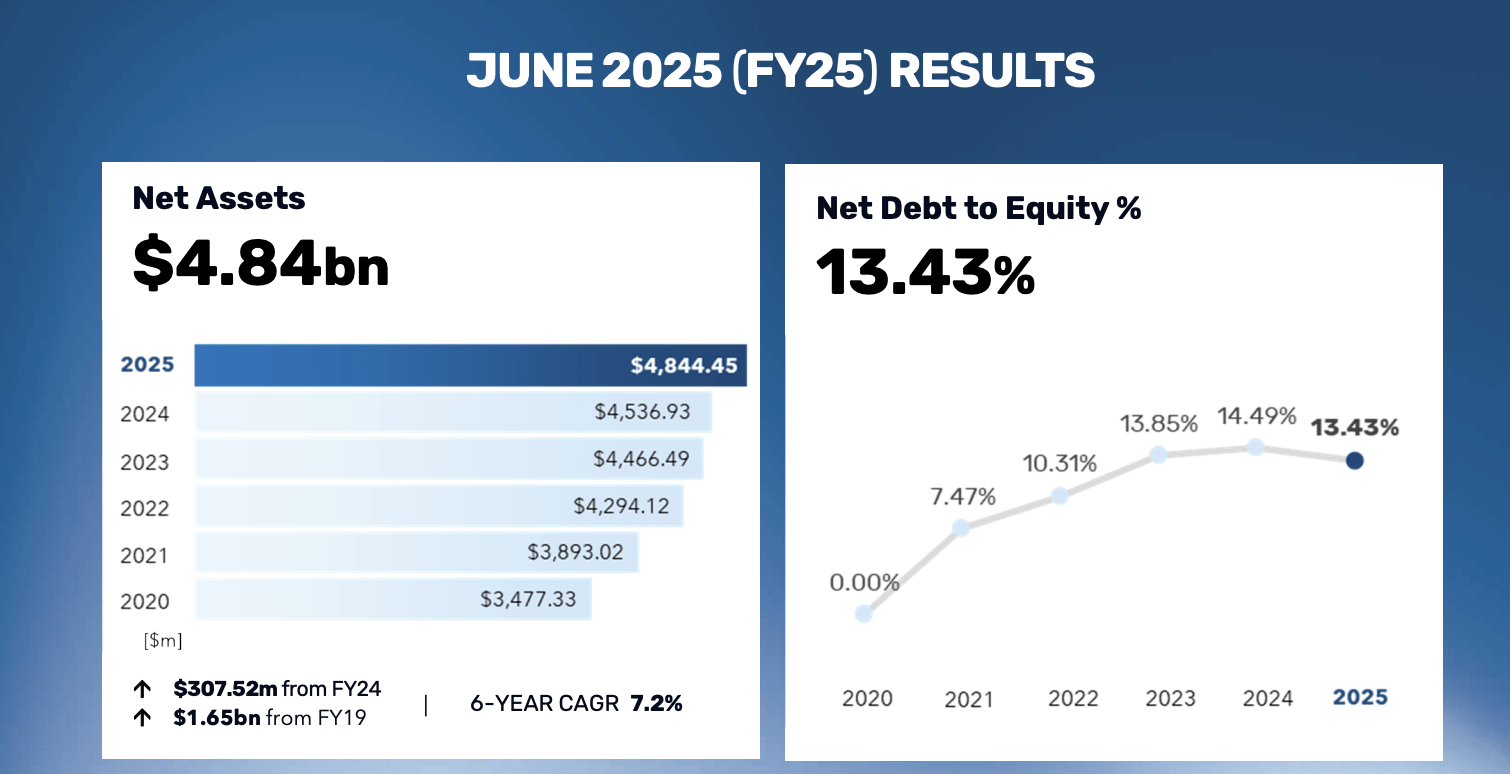

On the company’s own figures to 30 June 2025, total assets came in at $8.37 billion and net assets at $4.84 billion.

Management reported a net debt-to-equity ratio of 13.43%, which translates to around $650 million in net debt once cash holdings are deducted.

On that measure, the leverage appears moderate.

Taking only interest-bearing loans and borrowings, Harvey Norman had about $938 million in gross debt at year-end, offset by roughly $280 million in cash, giving net debt of $658.5 million.

But when accounting standards treat lease liabilities as debt-like obligations, the total rises steeply.

That puts Harvey Norman’s total debt closer to $2.3 billion, highlighting how much of its financing is tied to store leases and property holdings.

One way analysts gauge leverage is through the net debt-to-EBITDA ratio.

This compares borrowings with annual operating cash earnings before interest, tax, depreciation and amortisation.

Harvey Norman sits below one-times, meaning it could theoretically repay all net debt in less than a year if it applied all operating cash flow to the task.

Harvey Norman’s debt isn’t worrying – as long as there are no unpleasant surprises

Another safety check is interest coverage, which measures how easily earnings can meet financing costs.

Harvey Norman’s earnings before interest are more than ten times its interest expense, indicating plenty of breathing room at current profit levels.

Harvey Norman Chairman Gerry Harvey certainly doesn’t seem worried. He’s pointed out the company’s net debt to equity ratio had declined from last financial year, when it was 14.49%.

He also noted that Harvey Norman had “delivered strong growth across all core segments” and was well-positioned for “sustainable growth and sustainable value creation”.

That may well prove to be the case.

However, anything from another pandemic to an economic shock to geopolitical instability could rapidly change the playing field the retailer is currently operating on.

Electronics and furniture sales are among the first to feel pressure when households tighten budgets. Harvey Norman is heavily exposed to both categories.

If earnings soften or interest costs climb further, today’s conservative gearing could feel a lot more aggressive.

Likewise, the retailer’s $3.9 billion freehold property portfolio underpins the balance sheet and provides options.

But it also ties Harvey Norman’s fortunes to real estate values and refinancing conditions.