Kogan Shares Fall, Down 52% YTD As He Tries To Take On Media Companies To Prop Up Revenue

Kogan shares fell 2.01% today, leaving the online retailer down 52% for the year despite reporting improved headline results.

The Melbourne-based company posted an adjusted EBITDA of $10.1 million for the first four months of the 2026 financial year—down 31.3% compared with the same period last year. The steep decline was largely attributed to losses from its New Zealand subsidiary, Mighty Ape, which has widely been described as a “dud” acquisition for Kogan.

Ruslan Kogan, the company’s founder (seen above), still remains optimistic about the future.

He claims that key initiatives to prop up Mighty Ape’s recovery have largely been achieved, and he is confident that the subsidiary’s financial performance will return to profitability in the second half of FY26.

Chairman Greg Ridder told shareholders that the company had increased its customer base by 35% compared with last year, claiming Kogan “served” 3.5 million customers over the past 12 months. However, he did not disclose how many of these were repeat customers or how many unique customers the business serves annually.

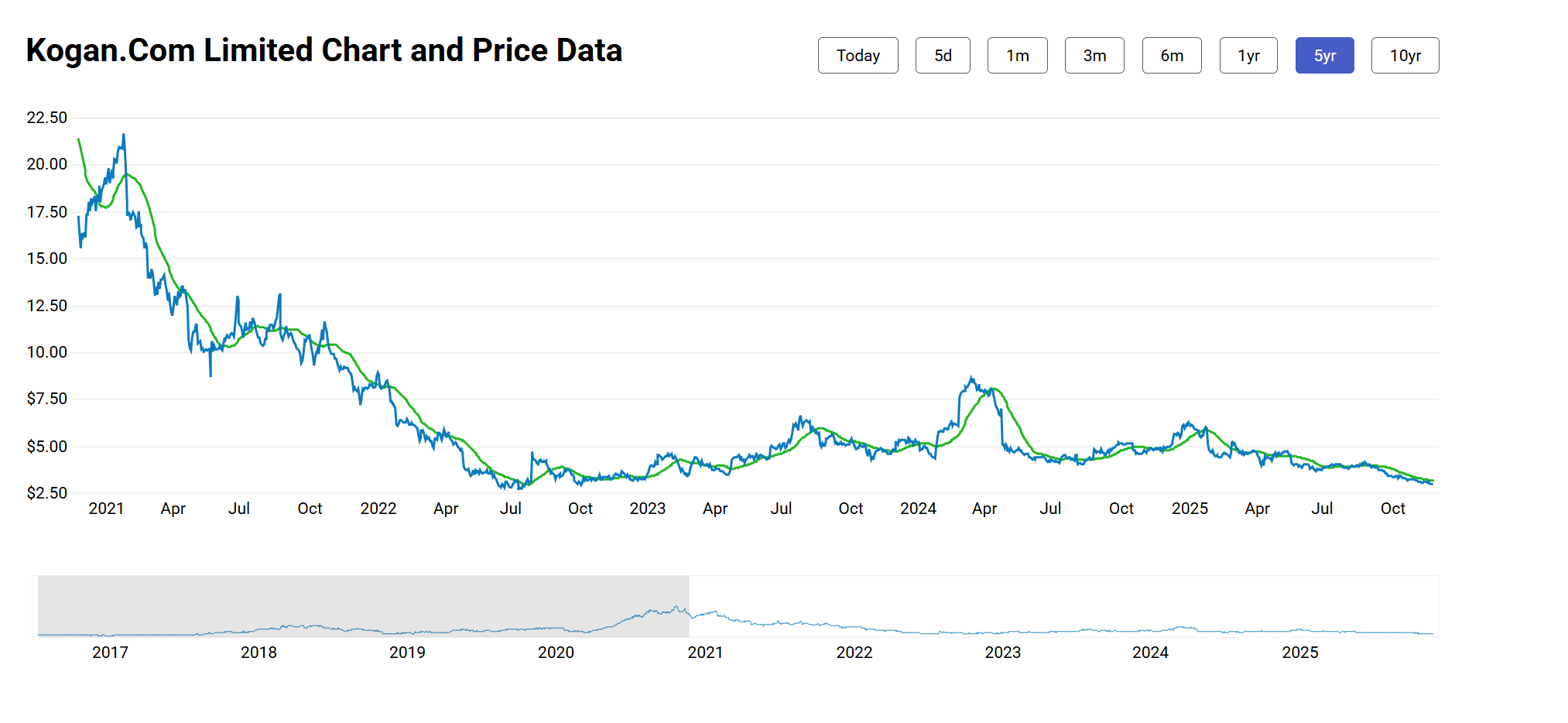

Since listing, Kogan’s share price has slid from $21.40 in 2017 to just $2.98 today.

As the company increasingly shifts into competition with media businesses to attract brand advertising dollars—whether through its marketplace or through brands it sells—Ridder said Kogan’s platform-based revenue streams, including marketplaces, loyalty programs, verticals, and advertising, generated $111.9 million last year.

Kogan’s own-brand products division recorded $258.1 million in revenue after the company “significantly rationalised its offering” in recent years. Ridder said the business is now focusing on core categories such as TVs, consumer electronics, furniture, and appliances. He also admitted Mighty Ape is performing “well below expectations.”

Under pressure from competitors like JB Hi-Fi and Amazon, Kogan has benefited from selling grey-imported products across key categories—a strategy that has delivered higher margins.

In the March quarter of 2024, the company reported a 5% decline in Australian gross sales compared with the same period the previous year, though recent growth has partly recovered previous losses.

For several quarters, Kogan has attempted a strategic pivot away from its early pure-play retail model toward marketplace, subscription, service revenue, and more recently, media-style advertising revenue. This shift comes despite founder Ruslan Kogan previously using traditional media outlets to promote the business. It also echoes his infamous 2016 prediction—made in a bet with then–JB Hi-Fi CEO Terry Smart—that “within three years JB Hi-Fi will be stopped from selling Apple computers,” a claim that proved entirely wrong.

Kogan has faced governance and regulatory controversies in the past, including an ASX investigation into a 2020 share-options deal involving Ruslan Kogan and CFO David Shafer. The timing of the option sales—just weeks before a significant share-price fall—raised questions about whether the board had appropriately considered material information.

Also in 2020, Kogan was fined A$350,000 by the Federal Court for misleading discount promotions.

Today, the company’s margins remain under pressure, and customer acquisition and retention costs are rising. While Kogan has attempted to diversify into services such as energy, mobile phone plans, NBN, and marketplace operations, analysts warn that these expansions carry operational risks and require scale the company has yet to achieve.

Kogan’s acquisition record has also been mixed. While it purchased the remnants of the collapsed Dick Smith online business, its bid for Wesfarmers’ Catch Group was unsuccessful, with Wesfarmers ultimately choosing to close the business rather than sell to Kogan.

The company has also dealt with inventory mismanagement and logistics problems in the pas