Google TV Growth Stalls As New Rivals Reshape European Market

Google TV continues to hold the largest share of the smart television platform market in Europe, but its expansion has slowed, with new competitors beginning to reshape the landscape, according to recent analysis from Omdia.

Software platforms are playing a bigger role in purchasing decisions, as they determine not only which apps and services are available but also how long devices remain supported. At the same time, companies behind these systems are increasingly influencing the direction of the industry, particularly in areas such as advertising and user data.

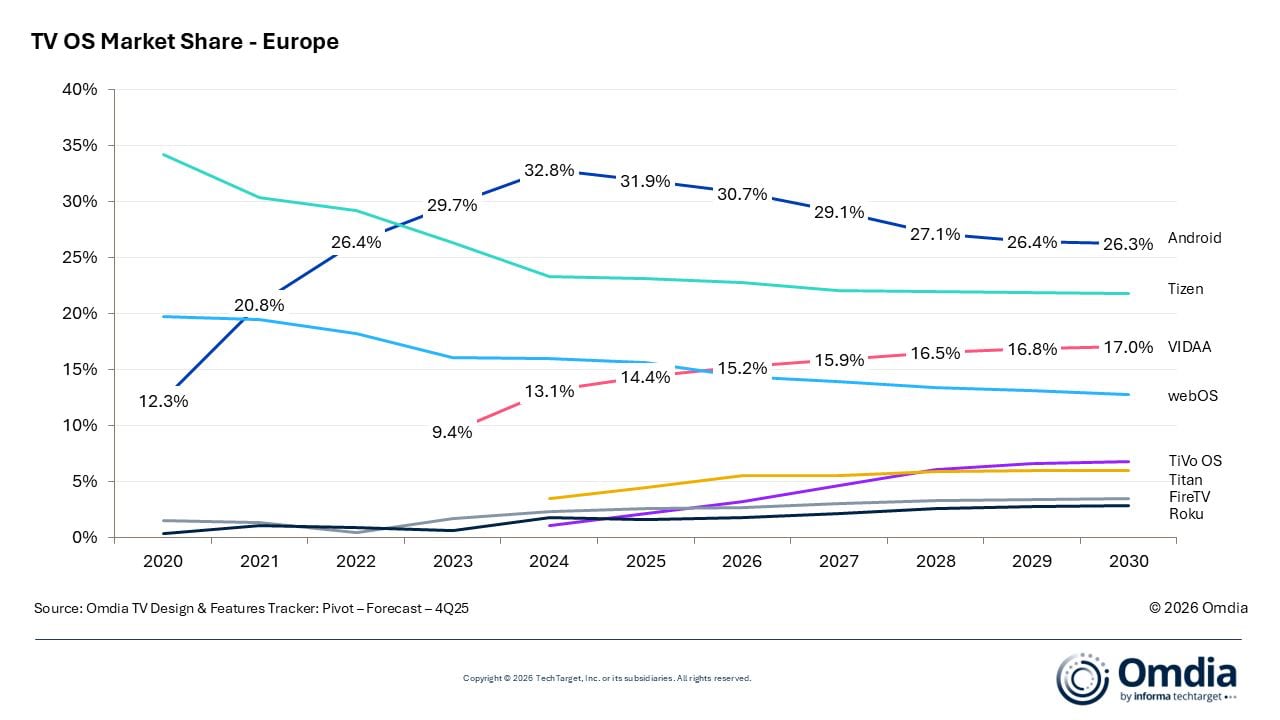

Google moved ahead of Samsung’s Tizen platform in 2022 and maintained its lead, but momentum has since tapered off. The platform reached its high point in 2024, after which growth began to ease as key partners started to shift away. Philips, operated by TP Vision, has been gradually replacing Google TV with its own Titan OS and is expected to complete that transition by 2026.

Omdia forecasts suggest Google’s Android TV ecosystem will remain the largest single platform in the region, though its share is expected to decline over time. Shipments accounted for roughly one in three units at their peak, with projections indicating a drop closer to one in four by the end of the decade. The shift reflects changes among manufacturers, with some major brands moving to alternative systems, leaving Google more reliant on partners such as TCL and smaller regional players.

The report also highlights a broader change in the competitive landscape, with South Korean brands facing increasing pressure from Chinese manufacturers. Companies like Hisense and TCL are not only gaining ground in hardware sales but are also expanding their own operating systems, challenging the established players.

Hisense’s Vidaa platform has already moved ahead of LG’s webOS in terms of adoption this year, signaling a notable shift in market dynamics. Meanwhile, newer systems are beginning to gain traction, including Titan OS and TiVo OS. Titan has been adopted by Philips, while TiVo is appearing in a growing number of lower-cost television models, including some from Panasonic.

In contrast, platforms that dominate in North America, such as Roku OS and Amazon’s Fire TV, have yet to achieve significant scale in Europe. The data focuses specifically on smart televisions and does not account for streaming devices, meaning some ecosystems may be underrepresented. Apple’s tvOS is also excluded from the analysis.

Looking ahead, Omdia’s projections extend through to 2030, though the outlook remains uncertain. Industry consolidation and shifting partnerships could play a major role, particularly as companies like TCL and Skyworth expand their influence through potential control of established television brands.